3% GDP Growth Elusive for Forever-Optimistic Economists

Friday, July 14, 2017 by Zelman & Associates

Filed under: Macro Housing

Having the responsibility of consistently predicting the future in a public forum is not for the faint of heart. Thus, we do not envy economists that are forced to opine on such far-reaching themes as energy, international trade, the consumer and housing, among many others. The last several years have been particularly difficult to predict given the unique nature of the financial crisis and extensive quantitative easing in response. With that said, economists have been far too optimistic over the last six years.

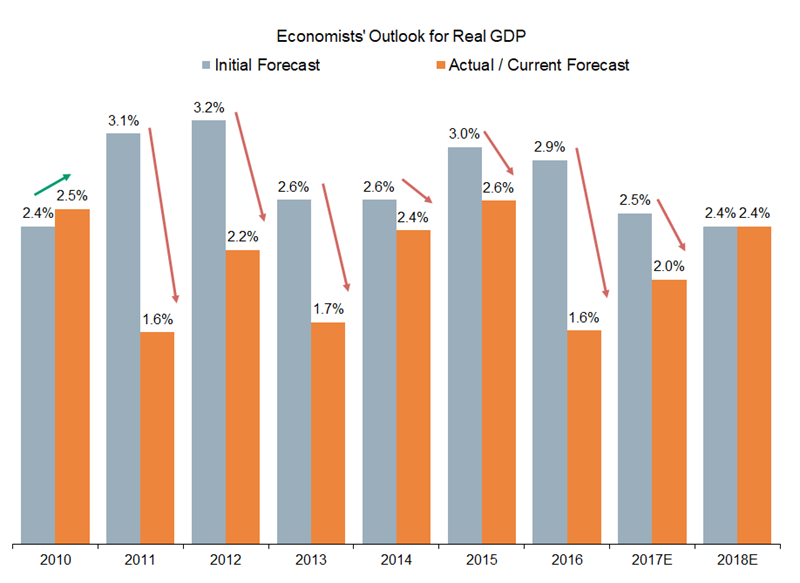

One way to track macro expectations is via Blue Chip Economic Indicators, which captures inputs from over 50 economists once a month. For 2010, these economists first published their outlook in January 2009, calling for 2.4% real GDP growth, on average. Actual results finished slightly stronger at 2.5%. However, each year since, the final economic production fell easily short of preliminary expectations. In 2011, 1.6% GDP growth compared to initial forecasts at 3.1%, representing the biggest miss over this period. Last year was not much better, with 1.6% growth disappointing early forecasts of 2.9%.

Over this six-year period, the initial outlook for real GDP has ranged from 2.6-3.2% while the final outcome has spanned 1.6-2.6%. Simplifying the analysis, economists hopefully anticipated near-term headwinds or “transitory factors” to fade, forecasting a return to 3% growth, only to find other headwinds fill the void and the economy subsequently trending closer to 2%.

For 2017, initial expectations were slightly more grounded, with the average forecast at 2.5% in January 2016, but disappointment has again surfaced as the average growth expectation is just 2.0% at present. Perhaps economists are beginning to doubt the ability of the economy to return to 3% growth, even with a tight employment situation, as the preliminary outlook for 2018 was the weakest since 2010 at just 2.4%, a level that has held since.

We question whether real GDP is the best measure of economic health, particularly with domestic activity having shifted so significantly to services from manufacturing. Nevertheless, it is a bogey often mentioned in the mainstream media regarding economic momentum and while optimism remains high for a politically-driven reversion back toward 3% growth, we suspect structural limitations on global growth will result in this year and next standing closer to 2% instead, once again.

Friday, July 14, 2017 by Zelman & Associates

Filed under: Macro Housing

Looking for More Insightful Content?

Explore our ResearchAffordabilityApartmentsBaby BoomersBuild-For-RentBuilding ProductsConstruction LendingConsumerDemographicsEntry-LevelExisting Home SalesHome ImprovementHome PricingHomebuildingHomeownershipHousehold FormationHousingHousing StartsInstitutional InvestorsInterest RatesM&AMacro HousingManufactured HousingMillennialsMortgageMortgage RatesNew Home SalesReal Estate ServicesRefinanceSG&ASingle-Family RentalStocksStudent DebtSupplySurvey