Is the "Pig in the Python" Back?

Thursday, June 24, 2021 by Ivy Zelman & Rachel Rockey

Filed under: AffordabilityExisting Home SalesHomeownershipHousingMacro HousingMortgageSupply

Most recently, the MBA reported that the number of borrowers in forbearance has dropped to 2.0 million – down from the peak of 4.3 million in June 2020. With forbearance expirations coming in the months ahead, many are concerned that these homes will eventually be dumped onto the market, shifting from an undersupply of listings to an oversupply in short order.

Many things are worth contemplating. Firstly, a portion of borrowers in forbearance plans have actually been paying their mortgage, with the MBA reporting that 24% of all borrowers that have exited forbearance plans since June 2020 had continued to make their payments while in forbearance. Secondly, mortgage servicers (and their regulators) will be laser-focused on modification efforts for those unable to resume their payments.

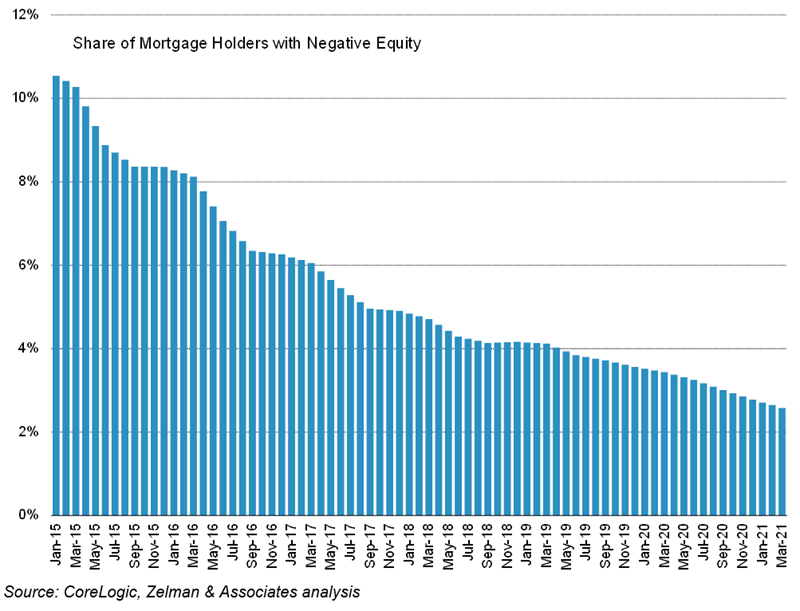

All else equal, amongst borrowers that have been unable to make their mortgage payments, those with less equity in their homes are likely at relatively higher risk. In particular, we would highlight delinquent FHA and VA loans originated in the past few years as more at-risk of foreclosure, as borrowers typically make lower down payments and have not had sufficient time to accumulate equity. Black Knight estimated that 885,000 FHA and VA loans were in forbearance as of mid-May, or 7% of that market. One step further, pre-COVID, there were approximately 170,000 FHA, VA and USDA borrowers in late-stage delinquency, or 1.5% of that market. In our view, the true foreclosure risk will likely be a number closer to the latter than the former.

It is important to remember the foreclosure process itself, one we all came to know too well during the Great Recession, is a highly involved and lengthy one. With the foreclosure moratorium bringing everything to a halt over a year ago, it may take a while to turn the plumbing back on since, in many cases, the human capital has been redeployed elsewhere. Furthermore, when the foreclosure process starts, depending on the state, the typical timeframe to completion is often 6-24 months – making the transition of foreclosed to for-sale inventory more akin to a trickle than a flood.

Combined with the resale market’s deficit of available inventory – down 19% year over year and 33% on a two-year basis – we continue to believe the market will be able to absorb the distressed homes that do end up flowing through the system. At the same time, the home price surge over the last two years has increased home equity for many, providing additional flexibility to at-risk borrowers. Specifically, with home prices up approximately 20% on a two-year basis, even borrowers who deferred their payments during COVID still likely amassed equity – even when factoring in said deferred repayments. Lastly, according to Black Knight, only 13% of total mortgages in forbearance have less than 10% equity in their home – which includes 23% of FHA/VA borrowers and 7% of GSE borrowers.

Thursday, June 24, 2021 by Ivy Zelman & Rachel Rockey

Filed under: AffordabilityExisting Home SalesHomeownershipHousingMacro HousingMortgageSupply

Looking for More Insightful Content?

Explore our ResearchAffordabilityApartmentsBaby BoomersBuild-For-RentBuilding ProductsConstruction LendingConsumerDemographicsEntry-LevelExisting Home SalesHome ImprovementHome PricingHomebuildingHomeownershipHousehold FormationHousingHousing StartsInstitutional InvestorsInterest RatesM&AMacro HousingManufactured HousingMillennialsMortgageMortgage RatesNew Home SalesReal Estate ServicesRefinanceSG&ASingle-Family RentalStocksStudent DebtSupplySurvey