Are Housing Demand and Supply Set on Diverging Courses?

Thursday, October 21, 2021 by Dennis McGill

Filed under: ApartmentsBuild-For-RentDemographicsHomebuildingHousing StartsMacro HousingSupply

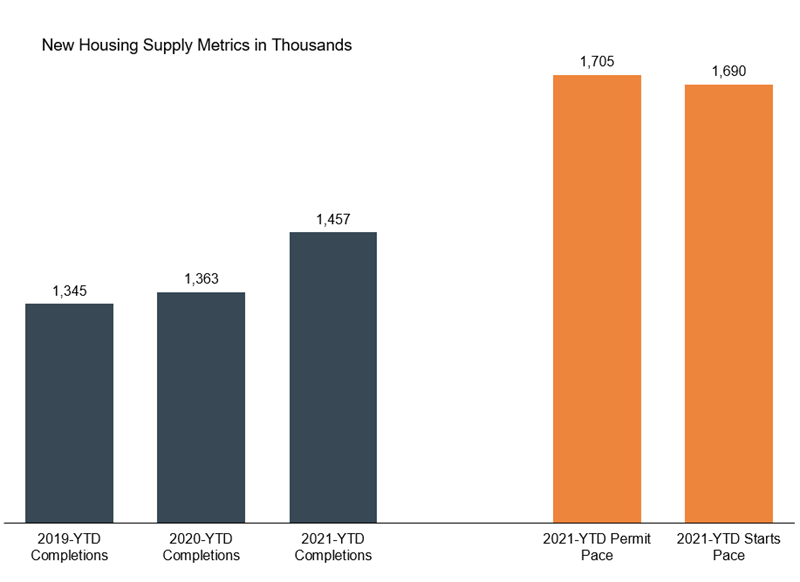

Through the first nine months of this year, approximately 1.45 million housing units were completed across single-family, multi-family and manufactured housing on a seasonally-adjusted basis. That was up only 7% year over year and was just 8% higher than the comparable period in 2019. With the pandemic unleashing much stronger demand for second homes and depleting available housing stock, such a level of new supply can be easily justified. However, pandemic effects, the frenzy created by plunging mortgage rates among existing households and many other distortions caused by government stimulus, eviction and foreclosure moratoriums, and excessive liquidity are very difficult to extrapolate, in our opinion.

Instead, developers’ actions are seemingly treating the demand boost as the new benchmark for growth. As compared to completions, which are backward looking, housing permits and starts provide a more useful future perspective. The pace of seasonally-adjusted permits, adjusted for the likelihood of being started, and starts have averaged closer to 1.70 million, or 17% higher than the pace of completions. Viewed differently, supply-side constraints that have extended construction cycles and a heavier concentration of multi-family projects has resulted in 1.45 million homes under construction, awaiting delivery to the market, which is higher than any month during the 2005-06 peak and the most since 1973. These are the seeds of oversupply we reference.

Beyond the supply already known to be coming to market over the next 6-12 months, optimism across homebuilders, single-family built-for-rent entities and multi-family developers amidst abundant capital willing to fund new projects strongly indicate that the current supply pace of 1.70 million is more likely to accelerate further, rather than retrench lower. Others with a more optimistic demand outlook or more confidence in an existing shortage will argue that this is necessary. We are more skeptical. With primary housing demand suffering as compared to pre-pandemic levels from lower employment, higher deaths and lower immigration, we believe that the risks to demand are not being fully appreciated.

Thursday, October 21, 2021 by Dennis McGill

Filed under: ApartmentsBuild-For-RentDemographicsHomebuildingHousing StartsMacro HousingSupply

Looking for More Insightful Content?

Explore our ResearchAffordabilityApartmentsBaby BoomersBuild-For-RentBuilding ProductsConstruction LendingConsumerDemographicsEntry-LevelExisting Home SalesHome ImprovementHome PricingHomebuildingHomeownershipHousehold FormationHousingHousing StartsInstitutional InvestorsInterest RatesM&AMacro HousingManufactured HousingMillennialsMortgageMortgage RatesNew Home SalesReal Estate ServicesRefinanceSG&ASingle-Family RentalStocksStudent DebtSupplySurvey